Cotton (Fr. coton; from Arab, qutun), the most important of the vegetable fibres of the world, consisting of unicellular hairs which occur attached to the seeds of various species of plants of the genus Gossypium, belonging to the Mallow order (Malvaceae). Each fibre is formed by the outgrowth of a single epidermal cell of the testa or outer coat of the seed.

Botany and Cultivation.—The genus Gossypium includes herbs and shrubs, which have been cultivated from time immemorial, and are now found widely distributed throughout the tropical and subtropical regions of both hemispheres. South America, the West Indies, tropical Africa and Southern Asia are the homes of the various members, but the plants have been introduced with success into other lands, as is well indicated by the fact that although no species of Gossypium is native to the United States of America, that country now produces over two-thirds of the world’s supply of cotton. Under normal conditions in warm climates many of the species are perennials, but, in the United States for example, climatic conditions necessitate the plants being renewed annually, and even in the tropics it is often found advisable to treat them as annuals to ensure the production of cotton of the best quality, to facilitate cultural operations, and to keep insect and fungoid pests in check.

Microscopic examination of a specimen of mature cotton shows that the hairs are flattened and twisted, resembling somewhat in general appearance an empty and twisted fire hose. This characteristic is of great economic importance, the natural twist facilitating the operation of spinning the fibres into thread or yarn. It also distinguishes the true cotton from the silk cottons or flosses, the fibres of which have no twist, and do not readily spin into thread, and for this reason, amongst others, are very considerably less important as textile fibres. The chief of these silk cottons is kapok, consisting of the hairs borne on the interior of the pods (but not attached to the seeds) of Eriodendron anfractuosum, the silk cotton tree, a member of the Bombacaceae, an order very closely allied to the Malvaceae.

|

| From Strasburger’s Lehrbuch der Botanik, by permission of Gustav Fischer. Fig. 1.—Seed-hairs of the Cotton, Gossypium herbaceum. A, Part of seed-coat with hairs; B1, insertion and lower part; B2, middle part; and B3, upper part of a hair. |

Classification.—Considerable difficulty is encountered in attempting to draw up a botanical classification of the species of Gossypium. Several are only known in cultivation, and we have but little knowledge of the wild parent forms from which they have descended. During the periods the cottons have been cultivated, selection, conscious or unconscious, has been carried on, resulting in the raising, from the same stock probably, in different places, of well-marked forms, which, in the absence of the history of their origin, might be regarded as different species. Then again, during at least the last four centuries, cotton plants have been distributed from one country to another, only to render still more difficult any attempt to establish definitely the origin of the varieties now grown. Under these circumstances it is not surprising to find that those who have paid attention to the botany of the cottons differ greatly in the number of species they recognize. Linnaeus described five or six species, de Candolle thirteen. Of the two Italian botanists who in comparatively recent years have monographed the group, Parlatore (Le Specie dei cotoni, 1866) recognizes seven species, whilst Todaro (Relazione sulla culta dei cotoni, 1877-1878) describes over fifty species: many of these, however, are of but little economic importance, and, in spite of the difficulties mentioned above, it is possible for practical purposes to divide the commercially important plants into five species, placing these in two groups according to the character of the hairs borne on the seeds. Sir G. Watt’s exhaustive work on Wild and Cultivated Cotton Plants of the World (1907) is the latest authority on the subject; and his views on some debated points have been incorporated in the following account.

A seed of “Sea Island cotton” is covered with long hairs only, which are readily pulled off, leaving the comparatively small black seed quite clean or with only a slight fuzz at the end, whereas a seed of “Upland” or ordinary American cotton bears both long and short hairs; the former are fairly easily detached (less easily, however, than in Sea Island cotton), whilst the latter adhere very firmly, so that when the long hairs are pulled off the seed remains completely covered with a short fuzz. This is also the case with the ordinary Indian and African cottons. There remains one other important group, the so-called “kidney” cottons in which there are only long hairs, and the seed easily comes away clean as with “Sea Island,” but, instead of each seed being separate, the whole group in each of the three compartments of the capsule is firmly united together in a more or less kidney-shaped mass. Starting with this as the basis of classification, we can construct the following key, the remaining principal points of difference being indicated in their proper places:—

|

i. Seeds covered with long hairs only, flowers yellow, turning to red. A. Seeds separate. Country of origin, Tropical America—(1) G. barbadense, L. B. Seeds of each loculus united. Country of origin, S. America—(2) G. brasiliense, Macf. ii. Seeds covered with long and short hairs. A. Flowers yellow or white, turning to red. a. Leaves 3 to 5 lobed, often large. Flowers white. Country of origin, Mexico—(3) G. hirsutum, L. b. Leaves 3 to 5, seldom 7 lobed. Small. Flowers yellow. Country of origin, India—(4) G. herbaceum, L. B. Flowers purple or red. Leaves 3 to 7 lobed. Place of origin, Old World—(5) G. arboreum, L. |

1. G. barbadense, Linn. This plant, known only in cultivation, is usually regarded as native to the West Indies. Watt regards it as closely allied to G. vitifolium, and considers the modern stock a hybrid, and probably not indigenous to the West Indies. He classifies the modern high-class Sea Island cottons as G. barbadense, var. maritima. Whatever may be its true botanical name it is the plant known in commerce as “Sea Island” cotton, owing to its introduction and successful cultivation in the Sea Islands and the coastal districts of South Carolina, Georgia and Florida. It yields the most valuable of all cottons, the hairs being long, fine and silky, and ranging in length from 3⁄8 to 2½ in. By careful selection (the methods of which are described below) in the United States, the quality of the product was much improved, and on the recent revival of the cotton industry in the West Indies American “Sea Island” seed was introduced back again to the original home of the species.

Egyptian cotton is usually regarded as being derived from the same species. Watt considers many of the Egyptian cottons to be races or hybrids of G. peruvianum, Cav. Egyptian cotton in length of staple is intermediate between average Sea Island and average Upland. It has, however, certain characteristics which cause it to be in demand even in the United States, where during recent years Egyptian cotton has comprised about 80% of all the “foreign” cottons imported. These special qualities are its fineness, strength, elasticity and great natural twist, which combined enable it to make very fine, strong yarns, suited to the manufacture of the better qualities of hosiery, for mixing with silk and wool, for making lace, &c. It also mercerizes very well. The principal varieties of Egyptian cotton are: Mitafifi, the best-known and most extensively grown, hardy and but little affected by climatic variation. It is usually regarded as the standard Egyptian cotton; the lint is yellowish brown, the seeds black and almost smooth, usually with a little tuft of short green hairs at the ends. Abassi, a variety comparatively recently obtained by selection. The lint is pure white, very fine and silky, but not so strong as Mitafifi cotton. Yannovitch, a variety known since about 1897, yields the finest and most silky lint of the white Egyptian cottons. Bamia, yielding a brown lint, very similar to Mitafifi, but slightly less valuable. Ashmouni, a variety principally cultivated in Upper Egypt. The lint is brown and generally resembles Mitafifi but is less valuable.

Other varieties are Zifiri, Hamouli and Gallini, all of minor importance.

2. G. brasiliense, Macf. (G. peruvianum, Engler), or kidney cotton. Amongst the varieties of cotton which are derived from this species appear to be Pernambuco, Maranham, Ceara, Aracaty and Maceio cottons. The fibre is generally white, somewhat harsh and wiry, and especially adapted for mixing with wool. The staple varies in length from 1 to about 1½ in.

3. G. hirsutum, Linn. Although G. barbadense yields the most valuable cotton, G. hirsutum is the most important cotton-yielding plant, being the source of American cotton, i.e. Upland, Georgia, New Orleans and Texas varieties. The staple varies usually in length between ¾ and 1¼ in. According to Watt there are many hybrids in American cottons between G. hirsutum and G. mexicanum.

4. G. herbaceum, Linn. Levant cotton is derived from this species. The majority of the races of cotton cultivated in India are often referred to this species, which is closely allied to G. hirsutum and has been regarded as identical with it. Amongst the cottons of this source are Hinganghat, Tinnevelly, Dharwar, Broach, Amraoti (Oomras or Oomrawattee), Kumta, Westerns, Dholera, Verawal, Bengals, Sind and Bhaunagar. Watt dissents from this view and classes these Indian cottons as G. obtusifolium and G. Nanking with their varieties. The Indian cottons are usually of short staple (about ¾ in.), but are probably capable of improvement.

5. G. arboreum, Linn. This species is often considered as indigenous to India, but Dr Engler has pointed out that it is found wild in Upper Guinea, Abyssinia, Senegal, etc. It is the “tree cotton” of India and Africa, being typically a large shrub or small tree. The fibre is fine and silky, of about an inch in length. In India it is known as Nurma or Deo cotton, and is usually stated to be employed for making thread for the turbans of the priests. Commercially it is of comparatively minor importance.

The following table, summarized from the Handbook to the Imperial Institute Cotton Exhibition, 1905, giving the length of staple and value on one date (January 16, 1905), will serve to indicate the comparative values of some of the principal commercial cottons. The actual value, of course, fluctuates greatly.

| Length of Staple. Inches. |

Value Per ℔. |

|

| Sea Island Cotton— | s. d. | |

| Carolina Sea Island | 1.8 | 1 3 |

| Florida Sea Island | 1.8 | 1 0 |

| Georgia Sea Island | 1.7 | 11¼ |

| Barbados Sea Island | 2.0 | 1 3 |

| Egyptian Cottons— | ||

| Yannovitch | 1.5 | 9¼ |

| Abassi | 1.5 | 8¾ |

| Good Brown Egyptian (Mitafifi) | 1.2 | 7½ |

| American Cotton— | ||

| Good middling Memphis | 1.3 | 42⁄5 |

| Good middling Texas | 1.0 | 41⁄5 |

| Good middling Upland | 1.0 | 4 |

| Indian Cottons— | ||

| Fine Tinnevelly | 0.8 | 4¼ |

| Fine Bhaunagar | 1.0 | 37⁄8 |

| Fine Amraoti | 1.0 | 37⁄8 |

| Fine Broach | 0.9 | 313⁄16 |

| Fine Bengal | 0.9 | 311⁄16 |

| Fine ginned Sind | 0.8 | 311⁄16 |

| Good ginned Kumta | 1.0 | 3½ |

The close relationship between the length of the staple and the market price will be at once apparent.

Cultivation.—Cotton is very widely cultivated throughout the world, being grown on a greater or less scale as a commercial crop in almost every country included in the broad belt between latitudes 43° N. and 33° S., or approximately within the isothermal lines of 60° F.

The cotton plant requires certain conditions for its successful cultivation; but, given these, it is very little affected by seasonal vicissitudes. Thus, for example, in the United States the worst season rarely diminishes the crop by more than about a quarter or one-third; such a thing as a “half-crop” is unknown. Various climatic factors may cause temporary checks, but the growing and maturing period is sufficiently long to allow the plants to overcome these disturbances.

Cotton requires for its development from six to seven months of favourable weather. It thrives in a warm atmosphere, even in a very hot one, provided that it is moist and that the transpiration is not in excess of the supply of water. An idea of the requirements of the plant will perhaps be afforded by summarizing the conditions which have been found to give the best results in the United States.

During April (when the seed is usually sown) and May frequent light showers, which keep the ground sufficiently moist to assist germination and the growth of the young plants, are desired. Three to four inches of rain per month is the average. The active growing period is from early June to about the middle of August. During June and the first fortnight in July plenty of sunshine is necessary, accompanied by sufficient rain to promote healthy, but not excessive, growth; the normal rainfall in the cotton belt for this period is about 4½ in. per month. During the second portion of July and the first of August a slightly higher rainfall is beneficial, and even heavy rains do little harm, provided the subsequent months are dry and warm. The first flowers usually appear in June, and the bolls ripen from early in August. Picking takes place normally during September and October, and during these months dry weather is essential. Flowering and fruiting go on continually, although in diminishing degree, until the advent of frost, which kills the flowers and young bolls and so puts an end to the production of cotton for the season.

In the tropics the essential requirements are very similar, but there the dry season checks production in much the same way as do the frosts in temperate climates. In either case an adequate but not excessive rainfall, increasing from the time of sowing to the period of active growth, and then decreasing as the bolls ripen, with a dry picking season, combined with sunny days and warm nights, provide the ideal conditions for successful cotton cultivation. In regions where climatic conditions are favourable, cotton grows more or less successfully on almost all kinds of soil; it can be grown on light sandy soils, loams, heavy clays and sandy “bottom” lands with varying success. Sandy uplands produce a short stalk which bears fairly well. Clay and “bottom” lands produce a large, leafy plant, yielding less lint in proportion. The most suitable soils are medium grades of loam. The soil should be able to maintain very uniform conditions of moisture. Sudden variations in the amount of water supplied are injurious: a sandy soil cannot retain water; on the other hand a clay soil often maintains too great a supply, and rank growth with excess of foliage ensues. The best soil for cotton is thus a deep, well-drained loam, able to afford a uniform supply of moisture during the growing period. Wind is another important factor, as cotton does not do well in localities subject to very high winds; and in exposed situations, otherwise favourable, wind belts have at times to be provided.

Cultivation in the United States.—The United States being the most important cotton-producing country, the methods of cultivation practised there are first described, notes on methods adopted in other countries being added only when these differ considerably from American practice.

The culture of cotton must be a clean one. It is not necessarily deep culture, and during the growing season the cultivation is preferably very shallow. The result is a great destruction of the humus of the soil, and great leaching and washing, especially in the light loams of the hill country of the United States. The main object, therefore, of the American cotton-planter is to prevent erosion. Wherever the planters have failed to guard their fields by hillside ploughing and terracing, these have been extensively denuded of soil, rendering them barren, and devastating other fields lying at a lower level, which are covered by the wash. The hillsides have gradually to be terraced with the plough, upon almost an exact level. On the better farms this is done with a spirit-level or compass from time to time and hillside ditches put in at the proper places. In the moist bottom-lands along the rivers it is the custom to throw the soil up in high beds with the plough, and then to cultivate them deep. This is the more common method of drainage, but it is expensive, as it has to be renewed every few years. More intelligent planters drain their bottom-lands with underground or open drains. In the case of small plantations the difficulties of adjusting a right-of-way for outlet ditches have interfered seriously with this plan. Many planters question the wisdom of deepbreaking and subsoiling. There can be no question that a deep soil is better for the cotton-plant; but the expense of obtaining it, the risk of injuring the soil through leaching, and the danger of bringing poor soil to the surface, have led many planters to oppose this plan. Sandy soils are made thereby too dry and leachy, and it is a questionable proceeding to turn the heavy clays upon the top. Planters are, as a result, divided in opinion as to the wisdom of subsoiling. Nothing definite can be said with regard to a rotation of crops upon the cotton plantation. Planters appreciate generally the value of broad-leaved and narrow-leaved plants and root crops, but there is an absence of exact knowledge, with the result that their practices are very varied. It is believed that the rotation must differ with every variety of soil, with the result that each planter has his own method, and little can be said in general. A more careful study of the physical as well as the chemical properties of a soil must precede intelligent experimentation in rotation. This knowledge is still lacking with regard to most of the cotton soils. The only uniform practice is to let the fields “rest” when they have become exhausted. Nature then restores them very rapidly. The exhaustion of the soil under cotton culture is chiefly due to the loss of humus, and nature soon puts this back in the excellent climate of the cotton-growing belt. Fields considered utterly used up, and allowed to “rest” for years, when cultivated again have produced better crops than those which had been under a more or less thoughtful rotation. In spite of the clean culture, good crops of cotton have been grown on some soils in the south for more than forty successive years. The fibre takes almost nothing from the land, and where the seeds are restored to the soil in some form, even without other fertilizers, the exhaustion of the soil is very slow. If the burning-up of humus and the leaching of the soil could be prevented, there is no reason why a cotton soil should not produce good crops continuously for an indefinite time. Bedding up land previous to planting is almost universal. The bed forms a warm seed-bed in the cool weather of early spring, and holds the manure which is drilled in usually to better advantage. The plants are generally left 2 or 3 in. above the middle of the row, which in four-foot rows gives a slope of 1 in. to the foot, causing the plough to lean from the plants in cultivating, and thus to cut fewer roots. The plants are usually cut out with a hoe from 8 to 14 in. apart. It seems to make little difference exactly what distance they are, so long as they are not wider apart on average land than 1 ft. On rich bottom-land they should be more distant. The seed is dropped from a planter, five or six seeds in a single line, at regular intervals 10 to 12 in. apart. A narrow deep furrow is usually run immediately in advance of the planter, to break up the soil under the seed. The only time the hoe is used is to thin out the cotton in the row; all the rest of the cultivation is by various forms of ploughs and so-called cultivators. The question of deep and shallow culture has been much discussed among planters without any conclusion applicable to all soils being reached. All grass and weeds must be kept down, and the crust must be broken after every rain, but these seem to be the only principles upon which all agree. The most effective tool against the weeds is a broad sharp “sweep,” as it is called, which takes everything it meets, while going shallower than most ploughs. Harrows and cultivators are used where there are few weeds, and the mulching process is the one desired.

The date of cotton-planting varies from March 1 to June 1, according to situation. Planting begins early in March in Southern Texas, and the first blooms will appear there about May 15. Planting may be done as late as April 15 in the Piedmont region of North Carolina, and continue as late as the end of May. The first blooms will appear in this region about July 15. Picking may begin on July 10 in Southern Texas, and continue late into the winter, or until the rare frost kills the plants. It may not begin until September 10 in Piedmont, North Carolina. It is a peculiarity of the cotton-plant to lose a great many of its blooms and bolls. When the weather is not favourable at the fruiting stage, the otherwise hardy cotton plant displays its great weakness in this way. It sheds its “forms” (as the buds are called), blooms, and even half-grown bolls in great numbers. It has frequently been noted that even well-fertilized plants upon good soil will mature only 15 or 20% of the bolls produced. No means are known so far for preventing this great waste. Experts are at an entire loss to form a correct idea of the cause, or to apply any effective remedy.

Cotton-picking is at once the most difficult and most expensive operation in cotton production. It is paid for at the rate of from 45 to 50 cents per cwt. of seed cotton. The work is light, and is effectually performed by women and even children, as well as men; but it is tedious and requires care. The picking season will average 100 days. It is difficult to get the hands to work until the cotton is fully opened, and it is hard to induce them to pick over 100 ℔ a day, though some expert hands are found in every cotton plantation who can pick twice as much. The loss resulting from careless work is very serious. The cotton falls out easily or is dropped. The careless gathering of dead leaves and twigs, and the soiling of the cotton by earth or by the natural colouring matter from the bolls, injure the quality. It has been commonly thought that the production of cotton in the south is limited by the amount that can be picked, but this limit is evidently very remote. The negro population of the towns and villages of the cotton country is usually available for a considerable share in cotton-picking. There is in the cotton states a rural population of over 7,000,000, more or less occupied in cotton-growing, and capable, at the low average of 100 ℔ a day, of picking daily nearly 500,000 bales. It is evident, therefore, that if this number could work through the whole season of 100 days, they could pick three or four times as much cotton as the largest crop ever made. Great efforts have been made to devise cotton-picking machines, but, as yet, complete success has not been attained. Lowne’s machine is useful in specially wide-planted fields and when the ground is sufficiently hard.

Cotton Ginning.—The crop having been picked, it has to be prepared for purpose of manufacture. This comprises separating the fibre or lint from the seeds, the operation being known as “ginning.” When this has been accomplished the weight of the crop is reduced to about one-third, each 100 ℔ of seed cotton as picked yielding after ginning some 33 ℔ of lint and 66 ℔ of cotton seed. The actual amounts differ with different varieties, conditions of cultivation, methods of ginning, &c.; a recent estimate in the United States gives 35% of lint for Upland cotton and 25% for Sea Island cotton as more accurate.

The separation of lint from seed is accomplished in various ways. The most primitive is hand-picking, the fibre being laboriously pulled from off each seed, as still practised in parts of Africa. In modern commercial cotton production ginning machines are always used. Very simple machines are used in some parts of Africa. The simplest cotton gin in extensive use is the “churka,” used from early times, and still largely employed in India and China. It consists essentially of two rollers either both of wood, or one of wood and one of iron, geared to revolve in contact in opposite directions; the seed cotton is fed to the rollers, the lint is drawn through, and the seed being unable to pass between the rollers is rejected. With this primitive machine, worked by hand, about 5 ℔ of lint is the daily output. In the Macarthy roller gin, the lint, drawn by a roller covered with leather (preferably walrus hide), is drawn between a metal plate called the “doctor” (fixed tangentially to the roller and very close to it) and a blade called the “beater” or knife, which rapidly moves up and down immediately behind, and parallel to, the fixed plate. The lint is held by the roughness of the roller, and the blade of the knife or beater readily detaches the seed from the lint; the seed falls through a grid, while the lint passes over the roller to the other side of the machine. A hand Macarthy roller gin worked by two men will clean about 4 to 6 ℔ of lint per hour. A similar, but larger machine, requiring about 1½ horse-power to run it, will turn out 50 to 60 ℔ of Egyptian or 60 to 80 ℔ of Sea Island cleaned cotton per hour. By simple modifications the Macarthy gin can be used for all kinds of cotton. Various attempts have been made to substitute a comb for the knife or beater, and one of the latest productions is the “Universal fibre gin,” in which a series of blunt combs working horizontally replace the solid beater and so-called knife of the Macarthy gin.

Opposed to the various types of roller gins is the “saw gin,” invented by Eli Whitney, an American, in 1792. This machine, under various modifications, is employed for ginning the greater portion of the cotton grown in the Southern States of America. It consists essentially of a series of circular notched disks, the so-called saws, revolving between the interstices of an iron bed upon which the cotton is placed: the teeth of the “saws”. catch the lint and pull it off from the seeds, then a revolving brush removes the detached lint from the saws, and creates sufficient draught to carry the lint out of the machine to some distance. Saw gins do considerable damage to the fibre, but for short-stapled cotton they are largely used, owing to their great capacity. The average yield of lint per “saw” in the United States, when working under perfect conditions, is about 6 ℔ per hour. Some of the American ginners are very large indeed, a number (Bulletin of the Bureau of the Census on Cotton Production) being reported as containing on the average 1156 saws with an average production of 4120 bales of cotton. Saw gins are not adapted to long-stapled cottons, such as Sea Island and Egyptian, which are generally ginned by machines of the Macarthy type.

The machine which will gin the largest quantity in the shortest time is naturally preferred, unless such injury is occasioned as materially to diminish the market value of the cotton. This has sometimes been to the extent of 1d. or 2d. per ℔ and even more as regards Sea Island and other long-stapled cottons. The production, therefore, of the most perfect and efficient cotton-cleaning machinery is of importance alike to the planter and manufacturer.

Baling.—The cotton leaves the ginning machine in a very loose condition, and has to be compressed into bales for convenience of transport. Large baling presses are worked by hydraulic power; the operation needs no special description. Bales from different countries vary greatly in size, weight and appearance. The American bale has been described in a standard American book on cotton as “the clumsiest, dirtiest, most expensive and most wasteful package, in which cotton or any other commodity of like value is anywhere put up.” Suggestions for its improvement, which if carried out would (it is estimated) result in a monetary saving of £1,000,000 annually, were made by the Lancashire Private Cotton Investigation Commission which visited the Southern States of America in 1906.

The approximate weights of some of the principal bales on the English market are as follows:—

| United States | 500 ℔ |

| Indian | 400 ℔ |

| Egyptian | 700 ℔ |

| Peruvian | 200 ℔ |

| Brazilian | 200 to 300 ℔ |

With baling the work of the producer is concluded.

Cultivation in Egypt.—Climatic conditions in Egypt differ radically from those in the United States, the rainfall being so small as to be quite insufficient for the needs of the plant, very little rain indeed falling in the Nile Delta during the whole growing season of the crop: yet Egypt is in order the third cotton-producing country of the world, elaborate irrigation works supplying the crop with the requisite water. The area devoted to cotton in Egypt is about 1,800,000 acres, and nine-tenths of it is in the Nile Delta. The delta soil is typically a heavy, black, alluvial clay, very fertile, but difficult to work; admixture of sand is beneficial, and the localities where this occurs yield the best cotton. Formerly in Egypt the cotton was treated as a perennial, but this practice has been generally abandoned, and fresh plants are raised from seed each year, as in America; one great advantage is that more than one crop can thus be obtained each year. The following rotation is frequently adopted. It should be noted that in Egypt the year is divided into three seasons—winter, summer and “Nili.” The two first explain themselves; Nili is the season in which the Nile overflows its banks.

| Winter. | Summer. | Nili. | |

| First year | Clover | Cotton | .. |

| Second year | Beans or wheat | .. | Corn or fallow |

For cotton cultivation the land is ploughed, carefully levelled, and then thrown up into ridges about 3 ft. apart. Channels formed at right angles to the cultivation ridges provide for the access of water to the crop. The seeds, previously soaked, are sown, usually in March, on the sides of the ridges, and the land watered. After the seedlings appear, thinning is completed in usually three successive hoeings, the plants being watered after thinning, and subsequently at intervals of from twelve to fifteen days, until about the end of August when picking commences. The total amount of water given is approximately equivalent to a rainfall of about 35 in. The crop is picked, ginned and baled in the usual way, the Macarthy style action roller gins being almost exclusively employed.

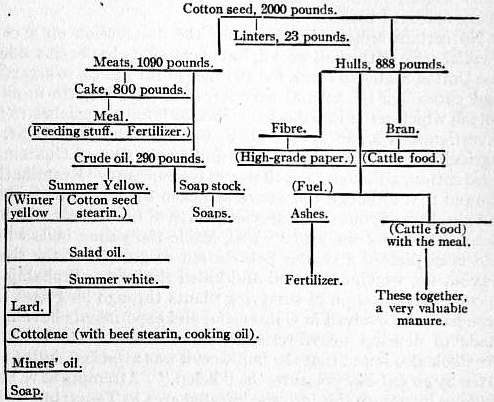

Cotton Seed.—The history of no agricultural product contains more of interest and instruction for the student of economics than does that of cotton seed in the United States. The revolution in its treatment is a real romance of industry. Up till 1870 or thereabouts, cotton seed was regarded as a positive nuisance upon the American plantation. It was left to accumulate in vast heaps about ginhouses, to the annoyance of the farmer and the injury of his premises. Cotton seed in those days was the object of so much aversion that the planter burned it or threw it into running streams, as was most convenient. If the seed were allowed to lie about, it rotted, and hogs and other animals, eating it, often died. It was very difficult to burn, and when dumped into rivers and creeks was carried out by flood water to fill the edges of the flats with a decaying and offensive mass of vegetable matter. Although used in the early days to a limited extent as a food for milch cows and other stock, and to a larger extent as a manure, no systematic efforts were made anywhere in the South to manufacture the seed until the later ’fifties, when the first cotton seed mills were established. It is said that there were only seven cotton oil mills in the South in 1860. The cotton-growing industry was interrupted by the Civil War, and the seed-milling business did not begin again until 1868. After that time the number of mills rapidly increased. There were 25 in the South in 1870, 50 in 1880, 120 in 1890, and about 500 in 1901, about one-third being in Texas.

Experience shows that 1000 ℔ of seed are produced for every 500 ℔ of cotton brought to market. On the basis, therefore, of a cotton crop of 10,000,000 bales of 500 ℔ each, there are produced 5,000,000 tons of cotton seed. If about 3,000,000 tons only are pressed, there remain to be utilized on the farm 2,000,000 tons of cotton seed, which, if manufactured, would produce a total of $100,000,000 from cotton seed. In contrast with the farmers of the ’sixties, the southern planter of the 20th century appreciates the value of his cotton seed, and farmers, too remote from the mills to get it pressed, now feed to their stock all the cotton seed they conveniently can, and use the residue either in compost or directly as manure. The average of a large number of analyses of Upland cotton seed gives the following figures for its fertilizing constituents:—Nitrogen, 3.07%; phosphoric acid, 1.02%; potash, 1.17%; besides small amounts of lime, magnesia and other valuable but less important ingredients. Sea Island cotton seed is rather more valuable than Upland: the corresponding figures for the three principal constituents being nitrogen 3.51, phosphoric acid 1.69, potash 1.59%. Using average prices paid for nitrogen, phosphoric acid and potash when bought in large quantities and in good forms, these ingredients, in a ton of cotton seed, amount to $9.00 worth of fertilizing material. Compared with the commercial fertilizer which the farmer has to buy, cotton seed possesses, therefore, a distinct value.

The products of cotton seed have become important elements in the national industry of the United States. The main product is the refined oil, which is used for a great number of purposes, such as a substitute for olive oil, mixed with beef products for preparation of compound lard, which is estimated to consume one-third of cotton seed oil produced in the States. The poorer grades are employed in the manufacture of soap, candles and phonograph records. Miners’ lamp oil consists of the bleached oil mixed with kerosene. Cotton seed cake or meal (the residue after the oil is extracted) is one of the most valuable of feeding stuffs, as the following simple comparison between it and oats and corn will show:—

| Average Analyses. | Proteins or Flesh Formers. |

Carbohydrates or Fuel and Fat Suppliers. |

Fats. | Ash or Bone Makers. |

| Cotton seed meal | 43.26 | 22.31 | 13.45 | 7.02 |

| Corn | 10.5 | 70.0 | 5.5 | 1.02 |

| Oats | 17.0 | 65.0 | 8.0 | 1.2 |

Cotton seed meal, though poor in carbohydrates, the fat- and energy-supplying ingredients, is exceedingly rich in protein, the nerve- and muscle-feeding ingredients. But it still contains a large amount of oil, which forms animal fat and heat, and thus makes up for part of its deficiency in carbohydrates. The meal, in fact, is so rich in protein that it is best utilized as a food for animals when mixed with some coarse fodder, thus furnishing a more evenly-balanced ration. In comparative valuations of feeding stuffs it has been found that cotton seed meal exceeds corn meal by 62%, wheat by 67%, and raw cotton seed by 26%. Cotton seed meal, in the absence of sufficient stock to consume it, is also used extensively as a fertilizer, and for this purpose it is worth, determining the price on the same basis as used above for the seed, from $19 to $20 per ton. But it has seldom reached this price, except in some of the northern states, where it is used for feeding purposes. A more rational proceeding would be to feed the meal to animals and apply the resulting manure to the soil. When this is done, from 80 to 90% of the fertilizing material of the meal is recovered in the manure, only 10 to 20% being converted by the animal into meat and milk. The profit derived from the 20% thus removed is a very large one. These facts indicate that we have here an agricultural product the market price of which is still far below its value as compared, on the basis of its chemical composition, either with other feeding stuffs or with other fertilizers. Though it is probably destined to be used even more extensively as a fertilizer before the demand for it as a feeding stuff becomes equal to the supply, practically all the cotton seed meal of the south will ultimately be used for feeding. One explanation of this condition of things is that there is still a large surplus of cotton seed which cannot be manufactured by the mills. Another reason is found in the absence of cattle in the south to eat it.

With the consideration of cotton seed oil and meal we have not, however, exhausted its possibilities. Cotton seed hulls constitute about half the weight of the ginned seed. After the seed of Upland cotton has been passed through a fine gin, which takes off the short lint or linters left upon it by the farmer, it is passed through what is called a sheller, consisting of a revolving cylinder, armed with numerous knives, which cut the seed in two and force the kernels or meats from the shells. The shells and kernels are then separated in a winnowing machine. This removal of the shell makes a great difference in the oilcake, as the decorticated cake is more nutritious than the undecorticated. For a long time these shells or hulls, as they are called, were burned at oil mills for fuel, 2½ tons being held equal to a cord of wood, and 41⁄3 tons to a ton of coal. The hulls thus burned produced an ash containing an average of 9% of phosphoric acid and 24% of potash—a very valuable fertilizer in itself, and one eagerly sought by growers of tobacco and vegetables. It was not long, however, before the stock-feeder in the South found that cotton seed hulls were an excellent substitute for hay. They are used on a very large scale in the vicinity of oil mills in southern cities like Memphis, New Orleans, Houston, and Little Rock, from 500 to 5000 cattle being often collected in a single yard for this purpose. No other feed is required, the only provision necessary being an adequate supply of water and an occasional allowance of salt. Many thousands of cattle are fattened annually in this way at remarkably low cost.

Careful attention is now given to the employment of the seed in new cotton countries, and oil expression is practised in the West Indies. Hull is the principal seat of the industry in Great Britain, and enormous quantities of Indian and Egyptian cotton seed are imported and worked up.

The following diagram, modified from one by Grimshaw, in accordance with the results obtained by the better class of modern mills, gives an interesting résumé of the products obtained from a ton of cotton seed:—

Products from a Ton of Cotton Seed.

Pests and Diseases of the Cotton Plant.

Insect Pests.—It is common knowledge that when any plant is cultivated on a large scale various diseases and pests frequently appear. In some cases the pest was already present but of minor importance. As the supply of its favourite food plant is increased, conditions of life for the pest are improved, and it accordingly multiplies also, possibly becoming a serious hindrance to successful cultivation. At other times the pest is introduced, and under congenial conditions (and possibly in the absence of some other organism which keeps it in check in its native country) increases accordingly. Some idea of the enormous damage wrought by the collective attacks of individually small and weak animals may be gathered from the fact that a conservative estimate places the loss due to insect attacks on cotton in the United States at the astounding figure of $60,000,000 (£12,000,000) annually. Of this total no less than $40,000,000 (£8,000,000) is credited to a small beetle, the cotton boll weevil, and to two caterpillars. The best means of combating these attacks depends on a knowledge of the life-histories and habits of the pests. The following notes deal only with the practical side of the question, and as the United States produce some seven-tenths of the world’s cotton crop attention is especially directed to the principal cotton pests of that country. Those of other regions are only referred to when sufficiently important to demand separate notice.

The cotton boll weevil (Anthonomus grandis), a small grey weevil often called the Mexican boll weevil, is the most serious pest of cotton in the United States, where the damage done by it in 1907 was estimated at about £5,000,000. It steadily increased in destructiveness during the preceding eight years. Attention was drawn to it in 1862, when it caused the abandonment of cotton cultivation about Monclova in Mexico. About 1893 it appeared in Texas, and then rapidly spread. It is easily transported from place to place in seed-cotton, and for this reason the Egyptian government in 1904 prohibited the importation of American cotton seed. Not only is the pest carried from place to place, but it also migrates, and in 1907 it crossed from Louisiana, where it first appeared in 1905, to Mississippi. That the insect is likely to prove adaptable is perhaps indicated by the fact that in 1906 it made a northward advance of about 60 m. in a season with no obvious special features favouring the pest. Its eastern progress was also rapid. “The additional territory infested during 1904 aggregates about 15,000,000 sq. m., representing approximately an area devoted to the culture of cotton of 900,000 acres” (Year-book, U.S. Dept. Agriculture, 1904). In 1906 the additional area invaded amounted to 1,500,000 acres (Ibid., 1906).

The adult weevils puncture the young flower-buds and deposit eggs; and as the grubs from the eggs develop, the bud drops. They also lay eggs later in the year in the young bolls. These do not drop, but as the grubs develop the cotton is ruined and the bolls usually become discoloured and crack, their contents being rendered useless.

No certain remedy is known for the destruction on a commercial scale of the boll weevil, but every effort has been made in the United States to check the advance of the insect, to ascertain and encourage its natural enemies, and to propagate races of cotton which resist its attacks. Special interest attaches to the investigations made by Mr O. F. Cook, of the U.S. Dept. of Agriculture, in Guatemala. The Indians in part of Guatemala raise cotton, although the boll weevil is abundant. Examination showed that although the weevil attacked the young buds these did not drop off, but that a special growth of tissue inside the bud frequently killed the grub. Also, inside the young bolls which had been pierced a similar proliferation or growth of the tissue was set up, which enveloped and killed the pest. Probably by unconscious selection of surviving plants through long ages this type has been evolved in Guatemala, and experiments have been made to develop weevil-resistant races in the United States. Mr Cook also found that the boll weevil was attacked, killed and eaten by an ant-like creature, the “kelep.” Attempts have been made to introduce this into the infested area in Texas; but owing to the winter proving fatal to the “kelep” its usefulness may be restricted to tropical and subtropical regions.

The cotton boll worm (Chloridea obsoleta, also known as Heliothis armiger) is a caterpillar. The parent moth lays eggs, from which the young “worms” hatch out. They bore holes and penetrate into flower-buds and young bolls, causing them to drop. Fortunately the “worms” prefer maize to cotton, and the inter-planting at proper times of maize, to be cut down and destroyed when well infested, is a method commonly employed to keep down this pest. Paris green kills it in its young stages before it has entered the buds or bolls. The boll worm is most destructive in the south-western states, where the damage done is said to vary from 2 to 60% of the crop. Taking a low average of 4%, the annual loss due to the pest is estimated at about £2,500,000, and it occupies second place amongst the serious cotton pests of the U.S.A. The boll worm is widely spread through the tropical and temperate zones. It may occur in a country without being a pest to cotton, e.g. in India it attacks various plants but not cotton. It has not yet been reported as a cotton pest in the West Indies.

The Egyptian boll worm (Earias insulana) is the most important insect pest in Egypt and occurs also in other parts of Africa. Indian boll worms include the same species, and the closely related Earias fabia, which also occurs in Egypt.

The cotton worm (Aletia argillacea)—also called cotton caterpillar, cotton army worm, cotton-leaf worm—is also one stage in the life-history of a moth. It is a voracious creature, and unchecked will often totally destroy a crop. In former years the annual damage done by it in the United States was assessed at £4,000,000 to £6,000,000. Dusting with Paris green is, however, an efficient remedy if promptly applied at the outset of the attack. The annual damage was in 1906 reduced to £1,000,000 to £2,000,000, and this on a larger area devoted to cotton than in the case of the estimate given above. It is the most serious pest of cotton in the West Indies. The Egyptian cotton worm is Prodenia littoralis.

The caterpillars (“cut worms”) of various species of Agrotis and other moths occur in all parts of the world and attack young cotton. They can be killed by spreading about cabbage leaves, &c., poisoned with Paris green.

Locusts, green-fly, leaf-bugs, blister mites, and various other pests also damage cotton, in a similar way to that in which they injure other crops.

The “cotton stainers,” various species of Dysdercus, are widely distributed, occurring for example in America, the West Indies, Africa, India, &c. The larvae suck the sap from the young bolls and seeds, causing shrivelling and reduction in quantity of fibre. They are called “stainers” because their excrement is yellow and stains the fibre; also if crushed during the process of ginning they give the cotton a reddish coloration. The Egyptian cotton seed bug or cotton stainer belongs to another genus, being Oxycarenus hyalinipennis. Other species of this genus occur on the west coast of Africa. They do considerable damage to cotton seed.

Fungoid Diseases.—“Wilt disease,” or “frenching,” perhaps the most important of the fungoid disease of cotton in the United States, is due to Neocosmospora vasinfecta. Young plants a few inches high are usually attacked; the leaves, beginning with the lower ones, turn yellow, and afterwards become brown and drop. The plants remain very dwarf and generally unhealthy, or die. The roots also are affected, and instead of growing considerably in length, branch repeatedly and give rise to little tufts of rootlets. There is no method known of curing this disease, and all that can be done is to take every precaution to eradicate it, by pulling up and burning diseased plants, isolating the infected area by means of trenches, and avoiding growing cotton, or an allied plant such as the ochro (Hibiscus esculentus), in the field. Fortunately the careful work of the U.S. Department of Agriculture and of planters such as Mr E. L. Rivers of James Island, South Carolina, has resulted in the production of disease-resistant races. In one instance Mr Rivers found one healthy plant in a badly affected field. The seed was saved and gave rise to a row of plants all of which grew healthily in an infected field, whereas 95% of ordinary Sea Island cotton plants from seed from a non-infected field planted alongside as a control were killed. The resistance was well maintained in succeeding generations, and races so raised form a practical means of combating this serious disease.

In “Root rot,” as the name implies, the roots are attacked, the fungus being a species of Ozonium, which envelops the roots in a white covering of mould or mycelium. The roots are prevented from fulfilling their function of taking up water and salts from the soil; the leaves accordingly droop, and the whole plant wilts and in bad attacks dies. It has yearly proved a more serious danger in Texas and other parts of the south-west of the United States, and the damage due to it in Texas during 1905 was estimated at about £750,000. No remedy is known for the disease, and cotton should not be planted on infected land for at least three or four years.

“Boll rot,” or “Anthracnose,” is a disease which may at times be sufficiently serious to destroy from 10 to 50% of the crop. The fungus which causes it (Colletotrichum gossypii) is closely related to one of the fungi attacking sugar-cane in various parts of the world. Small red-brown spots appear on the bolls, gradually enlarge, and develop into irregular black and grey patches. The damage may be only slight, or the entire boll may ripen prematurely and become dry and dead.

Many other diseases occur, but the above are sufficient to indicate some of the principal ones in the most important cotton countries of the world.

Improvement of Cotton by Seed Selection.

In the cotton belt of the United States it would be possible to put a still greater acreage under this crop, but the tendency is rather towards what is known as “diversified” or mixed farming than to making cotton the sole important crop. Cotton, however, is in increasing demand, and the problem for the American cotton planter is to obtain a better yield of cotton from the same area,—by “better yield” meaning an increase not only in quantity but also in quality of lint. This ideal is before the cotton grower in all parts of the world, but practical steps are not always taken to realize it. Some of the United States planters are alert to take advantage of the application of science to industry, and in many cases even to render active assistance, and very successful results have been attained by the co-operation of the United States Department of Agriculture and planters. With the improvement of cotton the name of Mr Herbert J. Webber is prominently associated, and a full discussion of methods and results will be found in his various papers in the Year-books of the U.S. Department of Agriculture. The principle on which the work is based is that plants have their individualities and tend to transmit them to their progeny. Accordingly a selection of particular plants to breed from, because they possess certain desirable characteristics, is as rational as the selection of particular animals for breeding purposes in order to maintain the character of a herd of cattle or of a flock of sheep.

Inspection of a field of cotton shows that different plants vary as regards productiveness, length, and character of the lint, period of ripening, power of resistance to various pests and of withstanding drought. A simple method of increasing the yield is that practised with success by some growers in the States. Pickers are trained to recognize the best plants, “that is, those most productive, earliest in ripening, and having the largest, best formed and most numerous bolls.” These pickers go carefully over the field, usually just before the second picking, and gather ripe cotton from the best plants only; this selected seed cotton is ginned separately, and the seed used for sowing the next year’s crop.

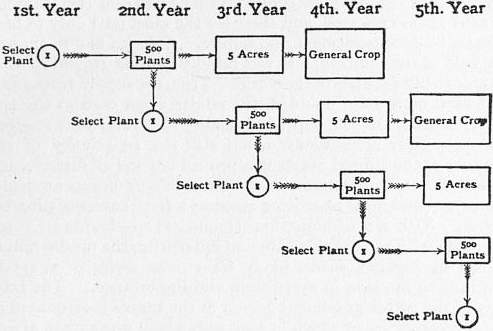

A more elaborate method of selection is practised by some of the Sea Island cotton planters in the Sea Islands, famous for the quality of their cotton. A field is gone over carefully, and perhaps some 50 of the best plants selected; a second examination in the field reduces these perhaps to one half, and each plant is numbered. The cotton from each is collected and kept separately, and at the end of the season carefully examined and weighed, and a final selection is then made which reduces the number to perhaps five; the cotton from each of these plants is ginned separately and the seed preserved for sowing. The simplest possible case in which only one plant is finally selected is illustrated in the diagram.

|

| After Webber, Year-book, U.S. Dept. of Agriculture, 1902. |

| Improvement of Cotton by Seed Selection. |

From the seeds of the selected plant of the 1st year about 500 plants can be raised in the next year. One plant is selected again from these 500, and the general crop of seed is used to sow about five acres for the 3rd year, from which seed is obtained for the general crop in the 4th year. One special plant is selected each year from the 500 raised from the previous season’s test plant, and in four years’ time the progeny of this plant constitutes the “general crop.” The practice may be modified according to the size of estate by selecting more than one plant each year, but the principle remains unaltered. This method is in actual use by growers of Sea Island cotton in America and in the islands off the coast of S. Carolina; the greatest care is taken to enhance the quality of the lint, which has been gradually improved in length, fineness and silkiness. Mr Webber, in summing up, says, “When Sea Island cotton was first introduced into the United States from the West Indies, it was a perennial plant, unsuited to the duration of the season of the latitude of the Sea Islands of S. Carolina; but, through the selection of seed from early maturing individual plants, the cotton has been rendered much earlier, until now it is thoroughly adapted to the existing conditions. The fibre has increased in length from about 1¾ to 2½ in., and the plants have at the same time been increased in productiveness. The custom of carefully selecting the seed has grown with the industry and may be said to be inseparable from it. It is only by such careful and continuous selection that the staple of these high-bred strains can be kept up to its present superiority, and if for any reason the selection is interrupted there is a general and rapid decline in quality.”

When selection is being made for several characters at the same time, and also in hybridization experiments, where it is important to have full records of the characters of individual plants and their progeny, “score cards,” such as are used in judging stock, with a scale of points, are used.

The improvements desired in cotton vary to some degree in different countries, according to the present character of the plants, climatic conditions, the chief pests, special market requirements, and other circumstances. Amongst the more important desiderata are:—

1. Increased Yield.

2. Increase in Length of Lint.—Webber records the case of Stamm Egyptian cotton imported into Columbia, in which by simple selection, as outlined above, during two years plants were obtained uniformly earlier, more productive, and yielding longer and better lint.

3. Uniformity in Length of the Lint.—This is important especially in the long-stapled cottons, unevenness leading to waste in manufacture, and consequently to a lower price for the cotton.

4. Strength of Fibre.—Long-stapled cottons have been produced in the States by crossing Upland and Sea Island cotton. These hybrids produce a lint which is long and silky, but often deficient in strength: selection for strength amongst the hybrids, with due regard to length, may overcome this.

5. Season of Maturing.—Seed should be selected from early and late opening bolls, according to requirements. Earliness is especially important in countries where the season is short.

6. Adaptation to Soil and Climate.—High-class cottons often do not flourish if introduced into a new country. They are adapted to special conditions which are lacking in their new surroundings, but a few will probably do fairly well the first year, and the seeds from these probably rather better the next, and so on, so that in a few years’ time a strain may be available which is equal or even superior to the original one introduced.

7. Resistance to Disease.—The method employed is to select, for seed purposes, plants which are resistant to the particular disease. Thus sometimes a field of cotton is attacked by some disease, perhaps “wilt,” and a comparatively few plants are but very slightly affected. These are propagated, and there are instances as described above of very successful and commercially important results having been attained. Special interest attaches to experiments made in the United States to endeavour to raise races of cotton resistant to the boll weevil.

8. Resistance to Weather.—Strong winds and heavy rains do much damage to cotton by blowing or beating the lint out of the bolls. In some instances a slight difference in the shape, mode of opening, &c., of the boll prevents this, and accordingly seed is selected from bolls which suffer least under the particular adverse conditions.

Attention has been paid in the West Indies to seed selection, by the officers of the imperial Department of Agriculture, with the object of retaining for West Indian Sea Island cotton its place as the most valuable cotton on the British market.

In India, where conditions are much more diversified and it is more difficult to induce the native cultivator to adopt new methods, attention has also been directed during recent years to the improvement of the existing races. Efforts have been made in the same direction in Egypt, West Africa, &c.

The World’s Commercial Cotton Crop.

It is impossible to give an exact return of the total amount of cotton produced in the world, owing to the fact that in China, India and other eastern countries, in Mexico, Brazil, parts of the Russian empire, tropical Africa, &c., considerable—in some eases very large—quantities of cotton are made up locally into wearing apparel, &c., and escape all statistical record. It is estimated that the amount thus used in India exclusive of the consumption of mills is equivalent to about 400,000 bales. Neglecting, however, these quantities, which do not affect the world’s market, the annual supplies of cotton are approximately as follows:—

| Country. | Approximate Production. Bales of 500 ℔. |

Percentage. |

| United States of America | 11,000,000 | 68.75 |

| India | 3,000,000 | 18.75 |

| Egypt | 1,000,000 | 6.25 |

| All other countries | 1,000,000 | 6.25 |

| Total | 16,000,000 | 100.00 |

In 1905 the world’s crop closely approximated to 16,000,000 bales, whilst in 1904 it was nearly 19,000,000 bales and in 1906 nearly 20,000,000 bales. The United States produced very nearly seven-tenths of the total “visible” cotton crops of the world. This, however, is quite a modern development, comparatively speaking. “During the period from 1786 to 1790 the West Indies furnished about 70% of the British supply, the Mediterranean countries 20%, and Brazil 8%; whilst the quantity contributed by the United States and India was less than 1% and Egypt contributed none. In 1906 the United States contributed 65% of the commercial cotton, British India 19%, Egypt 7%, and Russia 3%. Of the countries which were prominent in the production of cotton in 1790, Brazil and Asiatic Turkey alone remain” (U.S.A. Bureau of the Census, Bulletin No. 76). The actual figures for the chief countries for 1904-1906, taken from the same source, are as follows:—

The World’s Commercial Cotton Crop. (In 500 ℔ Bales.)

| Country. | 1904. | 1905. | 1906. |

| United States | 13,085,000 | 10,340,000 | 13,016,000 |

| British India | 2,843,000 | 2,519,000 | 3,708,000 |

| Egypt | 1,258,000 | 1,181,000 | 1,400,000 |

| Russia | 554,000 | 585,000 | 675,000 |

| China | 468,000 | 415,000 | 418,000 |

| Brazil | 210,000 | 258,000 | 275,000 |

| Mexico | 114,000 | 125,000 | 130,000 |

| Peru | 40,000 | 55,000 | 55,000 |

| Turkey | 100,000 | 107,000 | 107,000 |

| Persia | 45,000 | 47,000 | 47,000 |

| Japan | 16,000 | 15,000 | 11,000 |

| Other countries | 70,000 | 100,000 | 100,000 |

| Total | 18,803,000 | 15,747,000 | 19,942,000 |

This title serves to indicate the principal countries contributing to the world’s supply of cotton. The following notes afford a summary of the position of the industry in the more important countries.

| States and Territories. | Upland Cotton. | Sea Island Cotton. | Total Value. | ||

| Quantity. | Value. | Quantity. | Value. | ||

| ℔ | $ | ℔ | $ | $ | |

| Alabama | 603,651,989 | 60,425,564 | .. | .. | 60,425,564 |

| Arkansas | 450,991,361 | 45,144,235 | .. | .. | 45,144,235 |

| Florida | 17,876,133 | 1,789,401 | 9,031,896 | 2,587,638 | 4,377,039 |

| Georgia | 750,762,910 | 75,151,367 | 9,950,634 | 2,850,857 | 78,002,224 |

| Indian Territory | 196,648,765 | 19,684,542 | .. | .. | 19,684,542 |

| Kansas | 9,844 | 985 | .. | .. | 985 |

| Kentucky | 1,008,290 | 100,930 | .. | .. | 100,930 |

| Louisiana | 473,222,310 | 47,369,553 | .. | .. | 47,369,553 |

| Mississippi | 732,755,978 | 73,348,874 | .. | .. | 73,348,874 |

| Missouri | 26,040,093 | 2,606,613 | .. | .. | 2,606,613 |

| New Mexico | 74,340 | 7,442 | .. | .. | 7,442 |

| North Carolina | 276,215,506 | 27,649,172 | .. | .. | 27,649,172 |

| Oklahoma | 233,396,905 | 23,363,030 | .. | .. | 23,363,030 |

| South Carolina | 415,386,362 | 41,580,175 | 2,723,859 | 999,656 | 42,579,831 |

| Tennessee | 146,569,434 | 14,671,600 | .. | .. | 14,671,600 |

| Texas | 2,001,181,289 | 200,318,247 | .. | .. | 200,318,247 |

| Virginia | 6,609,963 | 661,657 | .. | .. | 661,657 |

| Total—United States | 6,332,401,472 | 633,873,387 | 21,706,389 | 6,438,151 | 640,311,538 |

| ( = 12,644,803 | .. | ( = 43,413 | .. | .. | |

| bales) | .. | bales) | .. | .. | |

United States of America.—The cultivation of cotton as a staple crop in the United States dates from about 1770,1 although efforts appear to have been made in Virginia as far back as 1621. The supplies continued to be small up to the end of the century. In 1792 the quantity exported from the United States was only equivalent to 275 bales, but by the year 1800 it had increased to nearly 36,000 bales. At the close of the war in 1815 the revival of trade led to an increased demand, and the progress of cotton cultivation in America became rapid and continuous, until at length about 85% of the raw material used by English manufacturers was derived from this one source. With a capacity for the production of cotton almost boundless, the crop which was so insignificant when the century began had in 1860 reached the enormous extent of 4,824,000 bales. This great source of supply, when apparently most abundant and secure, was shortly after suddenly cut off, and thousands were for a time deprived of employment and the means of subsistence. In this period of destitution the cotton-growing resources of every part of the globe were tested to the utmost; and in the exhibition of 1862 the representatives of every country from which supplies might be expected met to concert measures for obtaining all that was wanted without the aid of America. The colonies and dependencies of Great Britain, including India, seemed well able to grow all the cotton that could be required, whilst numerous other countries were ready to afford their co-operation. A powerful stimulus was thus given to the growth of cotton in all directions; a degree of activity and enterprise never witnessed before was seen in India, Egypt, Turkey, Greece, Italy, Africa, the West Indies, Queensland, New South Wales, Peru, Brazil, and in short wherever cotton could be produced; and there seemed no room to doubt that in a short time there would be abundant supplies independently of America. But ten years afterwards, in the exhibition of 1872, which was specially devoted to cotton, a few only of the thirty-five countries which had sent their samples in 1862 again appeared, and these for the most part only to bear witness to disappointment and failure. America had re-entered the field of competition, and was rapidly gaining ground so as to be able to bid defiance to the world. True, the supply from India had been more than doubled, the adulteration once so rife had been checked, and the improved quality and value of the cotton had been fully acknowledged, but still the superiority of the produce of the United States was proved beyond all dispute, and American cotton was again king. Slave labour disappeared, and under new and more promising auspices a fresh career of progress began. With rare combination of facilities and advantages, made available with remarkable skill and enterprise, the production of cotton in America seems likely for a long series of years to continue to increase in magnitude and importance. The total area of the cotton-producing region in the States is estimated at 448,000,000 acres, of which in 1906 only about one acre in fifteen was devoted to cotton. The potentialities of the region are thus enormous.

Cotton is now the second crop of the United States, being surpassed in value only by Indian corn (maize). The area devoted to this crop in 1879 was 14,480,019 acres, and the total commercial crop was 5,755,359 bales. In 1899 the acreage had increased to 24,275,101 and the crop to 9,507,786 bales. In 1906 the total area was 28,686,000 acres and the crop 13,305,265 bales.

The preceding table gives the quantity, value and character of the crop for each of the cotton-growing states in 1906, as reported by the Bureau of the Census.

Mexico.—Cotton is extensively grown in Mexico, and large quantities are used for home consumption. The cultivation is of very old standing. Cortes in 1519 is said to have received cotton garments as presents from the natives of Yucatan, and to have found the Mexicans using cotton extensively for clothing. From 1900 to 1905 the crop was about 100,000 bales per annum; the whole is consumed in local mills, and cotton is imported also from the United States.

Brazil.—The cotton-growing region in Brazil comprises a belt some 200 m. in width, in the north-eastern portion of the country, and a strip along the valley of the San Francisco, where a large amount of the present crop is produced. The cotton is known in commerce under the name of the place of export, e.g. Maceio, Pernambuco or Pernam, Ceãra, Rio Grande, &c. The export fluctuates greatly.

| Bales of 500 ℔. | Approx. Value. | |

| 1901 | 53,002 | £500,000 |

| 1902 | 143,963 | 1,200,000 |

| 1903 | 126,896 | 1,300,000 |

| 1904 | 59,413 | 800,000 |

| 1905 | 107,887 | 1,000,000 |

| 1906 | 142,972 | 1,500,000 |

The total production in 1906 was estimated at about 275,000 bales, but only a portion was available for export, there being an increasing consumption in Brazil itself.

Peru.—Cotton is an important crop in Peru, where it has long been cultivated. Most of the crop is grown in the irrigated coastal valleys. With more water available, the output could be considerably increased, e.g. in the Piura district. “Rough Peruvian,” the produce of one of the tree cottons, has a special use, as being rather harsh and wiry it is well adapted for mixing with wool. Egyptian cotton is also grown. The annual export is about 30,000 bales.

Cotton Production in the British West Indies: 1905-1906.2

| Island. | Area in Acres. |

Yield = Bales of 500 ℔. |

Average Price in Pence per ℔. |

Value of Lint and Seed. |

| Barbados. | 2,000 | 959 | 15.2 | £33,557 |

| St Vincent. | 790 | 330 | 18.0 | 13,557 |

| Grenada (mostly Marie galante cotton). | 3,600 | 623 | 5.0 | 8,400 |

| St Kitts | 1,000 | 241 | 15.0 | 8,380 |

| Nevis | 1,700 | 240 | 13.0 | 8,364 |

| Anguilla | 1,000 | 161 | 15.0 | 5,280 |

| Antigua | 700 | 200 | 14.2 | 6,522 |

| Montserrat | 770 | 196 | 15.0 | 6,789 |

| Virgin Islands | 40 | 14 | .. | 400 |

| Jamaica | 1,500 | 123 | .. | 4,025 |

| Total | 12,900 | 3087 | .. | £95,274 |

British West Indies.—Cotton was cultivated as a minor crop in parts of the West Indies as long ago as the 17th century, and at the opening of the 18th century the islands supplied about 70% of all the cotton used in Great Britain. Greater profits obtained from sugar caused the industry to be abandoned, except in the small island of Carriacou. In 1900 the Imperial Department of Agriculture and private planters began experiments with the object of reintroducing the cultivation, owing to the decline in value of sugar. The department was actively assisted by the British Cotton Growing Association, and the results have been very successful, as was shown at an exhibition held in Manchester in 1908. A supply of seed of a high grade of Sea Island cotton was obtained from Colonel Rivers’s estate in the Sea Islands, S. Carolina, and so successful has the cultivation been that from some of the islands West Indian Sea Island cotton obtains a higher price than the corresponding grade of cotton from the Sea Islands themselves.

In 1902 the total area under cotton cultivation in the British West Indies was 500 acres. The industry made rapid progress. In 1903 it was 4000; in 1905-1906 it was 12,900; and for 1906-1907 it was 18,166 acres. The table indicates the chief cotton-producing islands, the acreage in each, yield, average value per pound and total value of the crop in 1905-1906.

The whole of this crop was Sea Island cotton, with the exception of the “Marie galante” grown in Carriacou. Marie galante is a harsh cotton of the Peruvian or Brazilian type. The low yield per acre in this island, and also the low value of the lint per ℔ compared with the Sea Island cotton, is clearly apparent.

In 1906-1907 the acreage was substantially increased in many of the islands, e.g. Barbados from 2000 to 5000; St Vincent 790 to 1533; St Kitts and Anguilla 1000 to 1500 each; Antigua 700 to 1883. In Jamaica, on the other hand, it was reduced from 1500 to 300 acres.

Spain.—Cotton was formerly grown in southern Spain on an extensive scale, and as recently as during the American Civil War a crop of 8000 to 10,000 bales was obtained. It is considered that with facilities for irrigation Andalusia could produce 150,000 bales annually. The former industry was abandoned as other crops became more remunerative. The government is encouraging recent efforts to re-establish the cultivation.

Malta.—Cotton has long been cultivated in Malta, but the acreage diminished from 1750 acres in 1899 to 670 acres in 1906. A considerable quantity of the produce is spun and woven locally; e.g. in 1904 the export was equivalent to about 120 bales out of a total production of 330 bales, and in 1905 to 258 out of 333 bales (of 500 ℔ each).

Cyprus has a soil and climate suited to cotton, which was formerly grown here on a large scale. The rainfall is uncertain and low, however, never exceeding 40 in., and on the supply of water by irrigation the future of the industry mainly depends. The exports dwindled from 3600 bales in 1865 to 946 in 1905; great fluctuations occur, the export in 1904, for example, being only 338 bales. The cotton grown is rather short-stapled and goes mainly to Marseilles and Trieste. Some is used locally in the manufacture of cloth.

Egypt.—The position of Egypt as the third cotton-producing country of the world has already been pointed out, and the varieties grown and the mode of cultivation described. The introduction of the exotic varieties dates from the beginning of the 19th century. The industry was actively promoted by a Frenchman named Jumel, in the service of Mehemet Ali, from 1820 onwards with great success. The area under cotton is about 1,800,000 acres.

Cotton Production in Egypt.

| 1850 | 87,200 bales of 500 ℔. |

| 1865 | 439,000 ” ” |

| 1890 | 798,000 ” ” |

| 1904 | 1,258,000 ” ” |

| 1905 | 1,250,000 ” ” |

| 1906 | 1,400,000 ” ” |

The Egyptian Sudan.—Egyptian cotton was cultivated in the Sudan to the extent of 21,788 acres in 1906 chiefly on non-irrigated land. The exports, however, are small, almost all the crop being used locally. The chief difficulties are the supply of water, labour and transport facilities. Lord Cromer in his report on the Sudan for 1906 remarks that: “There seems to be some reason for thinking that the future—or at all events the immediate future—of Sudan agriculture lies more in the direction of cultivating wheat and other cereals than in that of cultivating cotton.”

West Africa.—Cotton has long been grown in the various countries on the west coast of Africa, ginned by hand or by very primitive means, spun into yarn, and woven on simple looms into “country cloths”; these are often only a few inches wide, so that any large cloths have to be made by sewing the narrow strips together. These native cloths are exceedingly durable, and many of them are ornamented by using dyed yarns and in other ways.

Southern Nigeria (Lagos) and northern Nigeria are the most important cotton countries amongst the British possessions on the coast. From the former there has been an export trade for many years which fluctuates remarkably according to the demand. Northern Nigeria is the seat of a very large native cotton industry, to supply the demand for cotton robes for the Mahommedan races inhabiting the country. The province of Zaria alone is estimated to produce annually 30,000 to 40,000 bales, all of which is used locally. Northern Nigeria contributes to the cotton exported from Lagos. The country offers a fairly promising field for development, especially now that arrangements have been made for providing the necessary means of transport by the construction of the new railways. The profits obtained from ground-nuts (Arachis hypogea) in Gambia, gold mining in the Gold Coast, and from products of the oil palm (Elaeis guineensis) in the palm-oil belt serve to prevent much attention being given to cotton in these districts.

Exports of Cotton from Lagos.

| 1865 | 868 bales of 500 ℔. |

| 1869 | 1785 ” ” |

| 1900 | 48 ” ” |

| 1901 | 15 ” ” |

| 1902 | 25 ” ” |

| 1903 | 582 ” ” |

| 1904 | 1725 ” ” |

| 1905 | 2578 ” ” |

Exports of Cotton from British West Africa, 1904, 1905 and 1906.

| 1904. | 1905. | 1906. | |

| Bales | Bales | Bales | |

| (500 ℔). | (500 ℔). | (500 ℔). | |

| Gambia | 120 | 5 | 0 |

| Sierra Leone | 56 | 139 | 176 |

| Gold Coast | 115 | 50 | 186 |

| Southern Nigeria and Lagos | 2296 | 2771 | 5392 |

| Northern Nigeria | 574 | 250* | 712 |

| Total | 3161 | 3215 | 6466 |

| *Approximately. | |||

Nyasaland (British Central Africa).—The cultivation of cotton on a commercial scale is quite new in Nyasaland, and although general conditions of soil and climate appear favourable the question of transport is serious and labour is not abundant. The exports were equivalent to 2 bales of 500 ℔ in 1902-1903, 114 bales in 1903-1904, 570 bales in 1904-1905, 1553 bales in 1905-1906 and 1052 bales in 1906-1907. In the lower river lands Egyptian cotton has been the most successful, whilst Upland cotton is more suited to the highlands.

British East Africa and Uganda.—In these adjoining protectorates wild cottons occur, and suitable conditions exist in certain localities. Experimental work has been carried on, and in 1904 Uganda exported about 43 bales of cotton, and British East Africa about 177 bales. In 1906 the combined exports had risen to 362 bales, including a little from German East Africa. In 1904-1905 there were some 300 acres under cotton in British East Africa. Lack of direct transport facilities is a difficulty. Some of the native cottons are of fair quality, but Egyptian cotton appears likely to be best suited for growing for export.

India is probably the most ancient cotton-growing country. For five centuries before the Christian era cotton was largely used in the domestic manufactures of India; and the clothing of the inhabitants then consisted, as now, chiefly of garments made from this vegetable product. More than two thousand years before Europe or England had conceived the idea of applying modern industry to the manufacture of cotton, India had matured a system of hand-spinning, weaving and dyeing which during that vast period received no recorded improvement. The people, though remarkable for their intelligence whilst Europe was in a state of barbarism, made no approximation to the mechanical operations of modern times, nor was the cultivation of cotton either improved or considerably extended. Possessing soil, climate and apparently all the requisite elements from nature for the production of cotton to an almost boundless extent, and of a useful and acceptable quality, India for a long series of years did but little towards supplying the manufactures of other countries with the raw material which they required. Between the years 1788 and 1850 numerous attempts were made by the East India Company to improve the cultivation and to increase the supply of cotton in India, and botanists and American planters were engaged for the purpose. One great object of their experiments was to introduce and acclimatize exotic cottons. Bourbon, New Orleans, Upland, Georgia, Sea Island, Pernambuco, Egyptian, &c., were tried but with little permanent success. The results of these and similar attempts led to the conclusion that efforts to improve the indigenous cottons were most likely to be rewarded with success. Still more recently, however, experiments have been made to grow Egyptian cotton in Sind with the help of irrigation. Abassi has given the best results, and the experiments have been so successful that in 1904-1905 an out-turn of not less than 100,000 bales “was prophesied in the course of a few years” (Report of Director, Land Records and Agriculture). The average annual production in India approximates to 3,000,000 bales. The area under cotton in all British India is about 20,000,000 acres, the crop being grown in a very primitive manner. The bulk of the cotton is of very short staple, about three-quarters of an inch, and is not well suited to the requirements of the English spinner, but very large mills specially fitted to deal with short-stapled cottons have been erected in India and consume about one-half the total crop, the remainder being exported to Germany and other European countries, Japan and China. In 1906 the United Kingdom took less than 5% of the cotton exported.

Cotton Production in British India.3

| 1859 | 1,316,800 bales of 500 ℔. |

| 1904 | 3,172,800 ” ” |

| 1905 | 2,848,800 ” ” |

| 1906 | 4,038,400 ” ” |

About 50% of the cotton produced is consumed in Indian mills and the remainder is exported.